“There are decades where nothing happens; and there are weeks when decades happen.”-Vladimir Lenin

“The last leg of a bull market always ends in hysteria; the last leg of a bear market always ends in panic.” – Jim Rogers

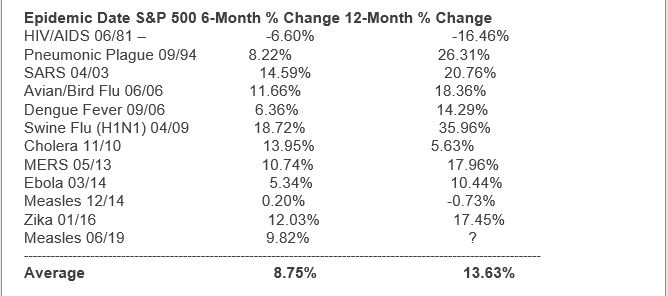

We are all aware of the pandemic but…do you remember the previous 14 over the last 40 years? Probably not. We recovered from them and we’ll recover from this.

But what CAN we DO?

- Minimize contact with groups; work & do schoolwork online.

- Go for walks, read a good book or The Good Book.

- Watch a favorite movie, VHS, DVD or online.

- If you play an instrument- practice. If you don’t, listen to music as it soothes the savage beast.

- Work on your taxes (returns may have been extended to July 15, but payment is still due April 15).

- If you’re eligible and haven’t made any ‘19 or ‘20 IRA contributions, consider doing so now.

- If possible, invest cash in a brokerage account and ‘buy low’.

- Take advantage of the warmer weather and start a vegetable garden.

- Don’t watch any more ‘news’ than usual- it’s not going to be real good for a while.