- Measure the performance of each investment in your portfolio. Many investments and investment managers will provide you with periodic performance information.

- Often, an investment’s return is reported on a time-weighted basis, which does not consider when you invested.

- Information that reports your portfolio’s return is generally expressed on a dollar-weighted basis, which measures the investment return based on when cash inflows and out-flows occurred. While this is a more relevant measure when evaluating your portfolio, time-weighted returns can make it easier to compare the returns of different investments.

- Investments often report cumu-lative annualized returns over a period of time, representing the aver-age annual performance over that

Continued on page 2

Frankly Speaking

Bear Markets HAPPEN!

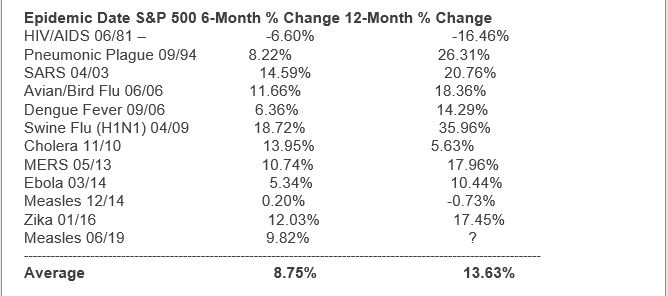

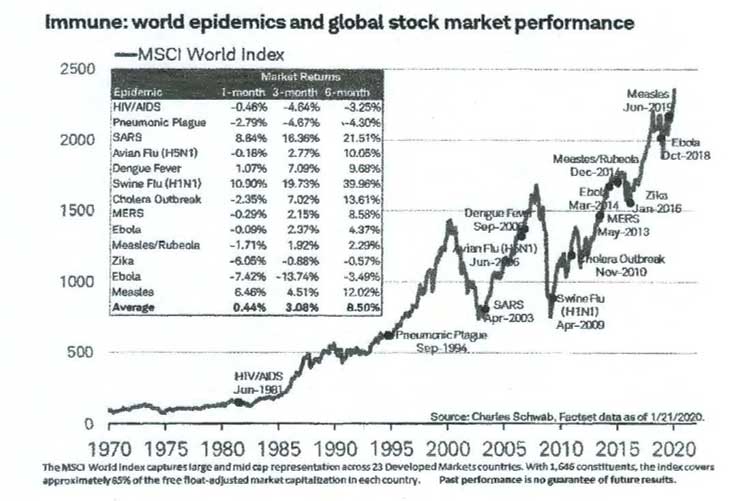

The Black Death killed 20 million Europeans in the 14th century. Venice, a major trade port, grew nervous. If a ship was suspected of harboring the plague, it had to wait 40 days before any passengers or goods could come ashore. Venice built a quarantine center on an island off its coast, where sailors from plague-infested ships were sent either to get better or, more likely, to die. This 40-day waiting period became known as quarantinario, from the Italian word for 40. – – NPR January 26, 2020

“The shortest period of time known to mankind is the time between when it is too soon to buy stocks and when it is too late.” – Mark Zinder

“Never let a good crisis go to waste.” – Winston Churchill

You may notice slight differences in this edition of Financial Success from my old newsletter. The latter was relatively generic while the former includes financial planning topics, from establishing goals and following economic trends to retirement, estate and tax planning, insurance and investments. A longer ‘sidebar’ will appear in the hard copy version and as an introduction to the HTML version. If you would like to see specific topics addressed, please let me know.

By now the Covid-19 or Wuhan virus has become as much a part of daily life as was the 10+ year stock market bull run in January. Did we really think it would last forever; that trees grew to the sky or that we had become so brilliant as to be impervious to the inevitability of periodic setbacks? Question is — did you re-balance your portfolio, shift some high performers to more conservative, fixed income-oriented positions or ‘guaranteed lifetime income accounts’*? Or has this ‘Black Swan’ event caught you entirely by surprise?

You may think there is no ‘getting back’ what you feel are losses, but if you haven’t sold or cashed out for CDs (Certificates of Depreciation), which offer less than the current rate of inflation.

PLEASE call or email me for a FREE no-cost, no-obligation consultation to see what we can do to improve your situation and create a brighter financial future for you and your family.

*Based on the claims paying ability of the issuing company

Copyright © 2020. Some articles in this newsletter were prepared by Integrated Concepts, a separate, nonaffiliated business entity. This newsletter intends to offer factual and up-to-date information on the subjects discussed but should not be regarded as a complete analysis of these subjects. Professional advisers should be consulted before implementing any options presented. No party assumes liability for any loss or damage resulting from errors or omissions or reliance on or use of this material.